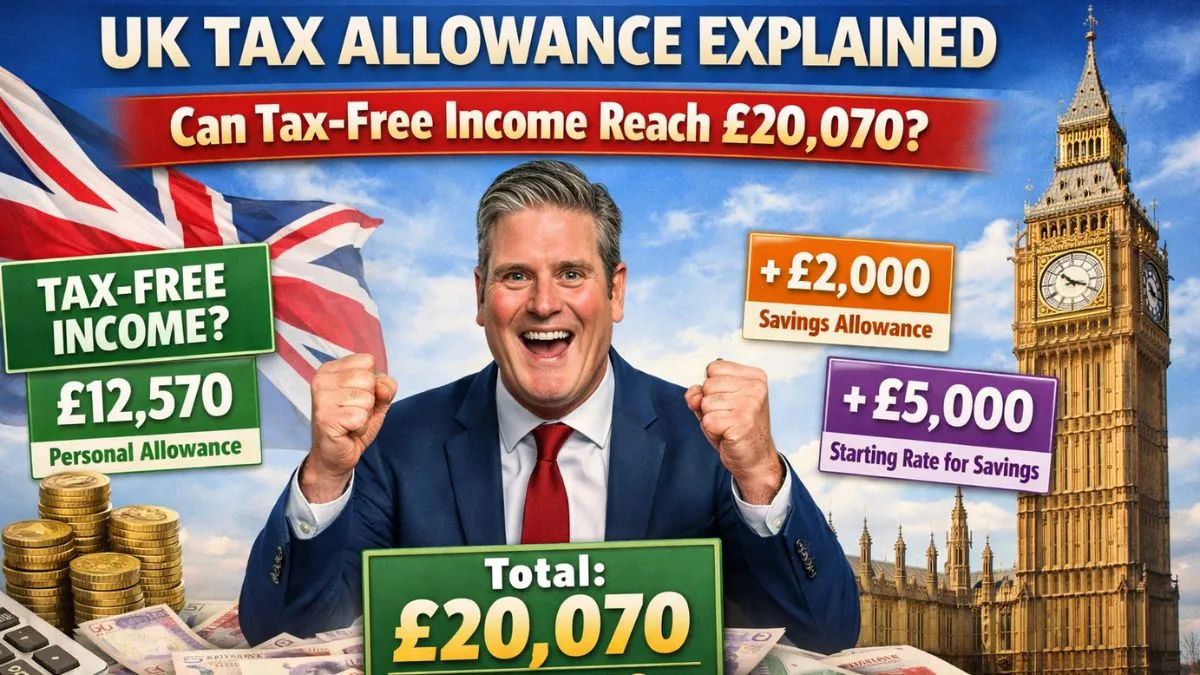

Understanding UK tax allowance rules is essential for workers, retirees, and anyone earning income in the United Kingdom. Recently, discussions around a possible tax-free income level of £20,070 have attracted significant attention. Many people believe this figure represents a new increase in the personal allowance, but the reality is slightly different.

In most cases, the UK tax allowance remains the standard personal allowance set by HMRC. However, certain individuals may legally receive income close to £20,070 without paying tax when several allowances are combined. These include savings allowances and special tax rules designed to support savers and retirees.

To fully understand this topic, it is important to explore how the UK tax allowance system works and how different tax-free thresholds interact.

What Is the Personal Allowance in the UK Tax System?

The personal allowance is the basic level of income that individuals in the UK can earn before paying income tax. It is one of the most important elements of the UK tax allowance framework.

This allowance applies to various types of income, including:

- Employment income

- Pension payments

- Certain other taxable earnings

The UK tax system is managed by HM Revenue and Customs, which is responsible for collecting taxes and administering tax regulations.

Once a person’s income exceeds their personal allowance, the remaining income becomes taxable according to the relevant tax bands.

Because of this, the UK tax allowance threshold plays a major role in determining how much tax someone must pay each year.

How Multiple Allowances Can Increase Tax-Free Income?

While the personal allowance sets the standard tax-free threshold, other tax rules can increase the amount of income someone receives without paying tax.

These additional allowances include:

- Starting rate for savings

- Personal savings allowance

When combined with the UK tax allowance, these rules can significantly raise the total income someone may receive tax-free.

For individuals with both earnings and savings interest, these allowances may increase their overall tax-free income close to figures such as £20,070.

However, this does not mean the official UK tax allowance itself has increased to that amount.

Understanding the Personal Savings Allowance

The personal savings allowance allows individuals to receive interest from savings without paying tax on that income.

The amount of savings interest that can be received tax-free depends on the person’s tax band.

Savings Allowance by Tax Band

| Taxpayer Type | Tax-Free Savings Interest |

|---|---|

| Basic rate taxpayers | Up to £1,000 |

| Higher rate taxpayers | Up to £500 |

| Additional rate taxpayers | £0 |

This allowance was introduced to encourage people to save money while simplifying how savings interest is taxed.

For many individuals, especially those with moderate savings, this allowance can significantly reduce tax payments.

What Is the Starting Rate for Savings?

Another important element of the UK tax allowance system is the starting rate for savings.

This rule is designed for people whose non-savings income is relatively low.

In these cases, savings interest can be taxed at a special starting rate, which may effectively reduce the tax owed on that interest to zero.

When the following allowances combine:

- Personal allowance

- Starting rate for savings

- Personal savings allowance

The total tax-free income can rise significantly for some individuals.

That is why figures such as £20,070 tax-free income sometimes appear in financial discussions.

Why Pensioners Often Benefit From These Tax Rules?

Retirees are among the groups most likely to benefit from the interaction of these allowances.

Many pensioners receive income from multiple sources, including:

- State Pension

- Workplace pensions

- Private pension savings

- Interest from savings accounts

Because some retirees have moderate income levels, they may qualify for additional allowances that increase their UK tax allowance threshold.

For many pensioners, this means a larger portion of their retirement income may remain tax-free.

How Tax Codes Affect the Amount of Tax You Pay?

The tax code system ensures that the correct amount of tax is deducted from wages or pension payments throughout the year.

Each taxpayer receives a tax code from HMRC, which reflects:

- Their personal allowance

- Any adjustments required for additional income

- Previous tax underpayments or overpayments

For people with multiple income sources, such as employment and pensions, tax codes may change to ensure the correct amount of tax is collected.

Sometimes these adjustments cause confusion, particularly if deductions appear unexpectedly in payslips or pension payments.

However, these changes are usually part of routine tax administration rather than new tax rules.

Financial Support Available for Pensioners

Although tax allowances can reduce tax liability, some pensioners may still need additional financial support.

One of the most important support schemes is Pension Credit.

This benefit helps increase the income of pensioners whose earnings fall below a certain threshold.

Receiving Pension Credit can also unlock additional support such as:

- Housing assistance

- Help with energy costs

- Other financial benefits

Unfortunately, many eligible pensioners do not claim Pension Credit and therefore miss out on valuable financial assistance.

Why Understanding the UK Tax Allowance Matters?

The UK tax allowance system includes several rules and allowances that can affect how much tax people pay.

Understanding these rules can help taxpayers:

- Reduce their tax liability

- Manage their finances more efficiently

- Maximize available allowances

For individuals with savings income or multiple sources of income, combining allowances correctly may allow them to keep more of their earnings.

Financial awareness is therefore essential when navigating the UK tax system.

Managing Income During Retirement

Retirement often changes how people receive income.

Instead of a single salary, retirees usually rely on multiple financial sources.

Common retirement income sources include:

- State pension payments

- Workplace pensions

- Private pension funds

- Savings interest

Understanding how each income source interacts with the UK tax allowance helps retirees manage their finances more effectively.

Many financial advisors recommend reviewing tax allowances regularly to ensure all available benefits are being used.

Why Tax Headlines Can Be Misleading

Headlines about tax changes often focus on specific figures that can be misunderstood.

For example, reports mentioning £20,070 tax-free income might suggest that everyone receives that allowance automatically.

In reality, the standard UK tax allowance remains separate from additional savings allowances.

The higher figure typically represents an example of combined allowances, not a universal tax-free threshold.

Understanding this distinction helps avoid confusion when reading tax-related news.

Important Points Taxpayers Should Remember

Key facts about the UK tax allowance include:

- The personal allowance determines basic tax-free income.

- Additional allowances may increase tax-free income for some people.

- Savings interest allowances can reduce tax liability.

- Pensioners with savings may benefit most from these rules.

- Tax codes ensure the correct tax amount is deducted.

The UK tax allowance system includes several rules that determine how much income individuals can earn before paying tax. While the standard personal allowance remains the main tax-free threshold, additional savings allowances can increase the total tax-free income available to some people.

This is why figures such as £20,070 occasionally appear in tax discussions. Rather than representing a new universal allowance, the number usually reflects how multiple allowances can combine under certain circumstances.

For workers, savers, and pensioners alike, understanding the UK tax allowance structure is essential for managing finances effectively. By staying informed about personal allowances, savings rules, and available benefits, taxpayers can make smarter financial decisions and maximize their income.

FAQs

1. Has the UK personal allowance increased to £20,070?

No. The official UK tax allowance has not increased to £20,070. That figure usually represents combined allowances such as savings allowances.

2. Who can benefit from higher tax-free income levels?

Individuals with low earnings and savings income, particularly pensioners, may benefit when multiple allowances combine under the UK tax rules.

3. What is the personal savings allowance?

The personal savings allowance lets basic-rate taxpayers earn up to £1,000 in savings interest tax-free, while higher-rate taxpayers receive £500.